Your Fund, That Fund-- All Funds Are Top Quartile!

Why Being A Top Quartile Fund Is Actually Meaningless

Listen to enough pitches and it seems like all GPs are in the top quartile. But how can almost all GPs be in the top quartile, if by definition the quartile signifies the top 25%?

When a fund tells me they are top quartile, I take it with a grain of salt. Why? Because it’s so easy to manipulate data to show that a fund is a top quartile. This is especially true for funds that are less than 5 years old. It’s why almost all GPs I speak to boast about their funds being amongst the best.

How?

Some GPs call themselves a top quartile GP despite only one fund being top quartile. Technically true, but misleading.

Others chose the benchmark (Pitchbook, Cambridge, Preqin, etc.) that puts their fund in the top quartile for their vintage. Because the funds in each dataset are different, performance numbers will be different. Sometimes, it’s by little, other times, enough to make a difference between the top quartile or some other quartile.

Some funds talk about their top quartile returns in terms of TVPI, others in MOIC, IRR, or DPI. If you get to pick and choose the metric, it becomes hard to not be a top quartile fund.

Numbers speak for themselves. I think intuitively (or through internal data that an institutional LP has), most LPs will have a rough idea of where a fund is positioned at a given point in time. In other words, a GP can tell their story with their data, but most LPs will see through it (I hope so anyway) and see what the GP performance for what it is.

For all the GPs with top quartile track records having a hard time raising, it could be because LPs can’t reconcile the GP's story with the actual reality.

All of this said, of course, there’s nothing wrong with a GP trying to put their best foot forward when pitching. If saying that they are top quartile helps, then, by all means, do so. Just don’t be surprised when there are a lot of passes even with a “top quartile” track record.

Are Too Many Private Equity Funds Top Quartile?

You don’t have to take my word for any of the above. There’s a really interesting study published in 2012 by Robert Harris at the University of Virginia and Tim Jenkinson and Rüdiger Stucke at the University of Oxford on just this:

“Using three popular data sources and applying metrics typically adopted in the industry, the authors demonstrate that even modest variations in methods can result in half of all funds being able to claim “top quartile” results. Sources of variation include methods of categorizing funds, definitions of vintage year, choice of the data source, specification of performance metrics, and treatment of geography and currencies.”

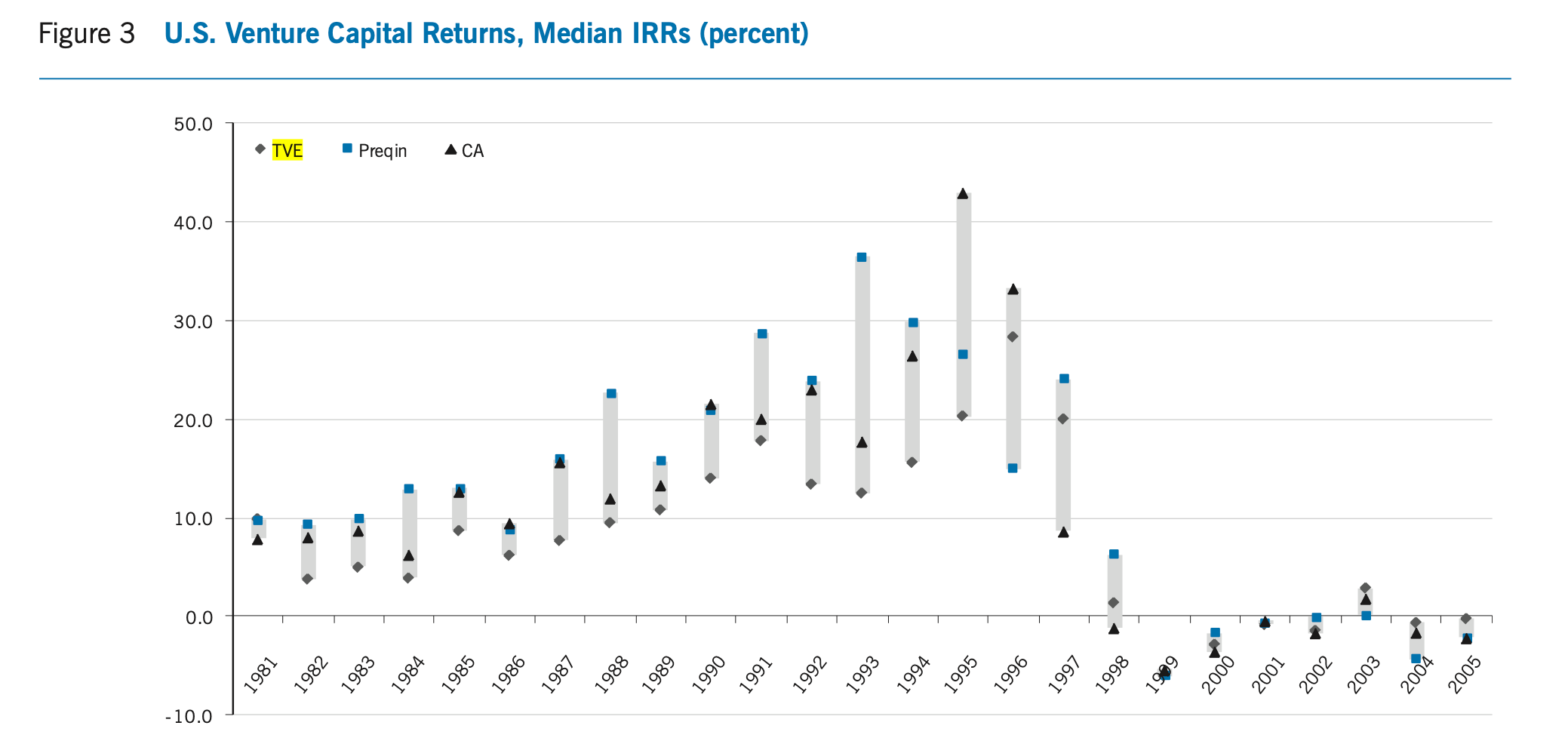

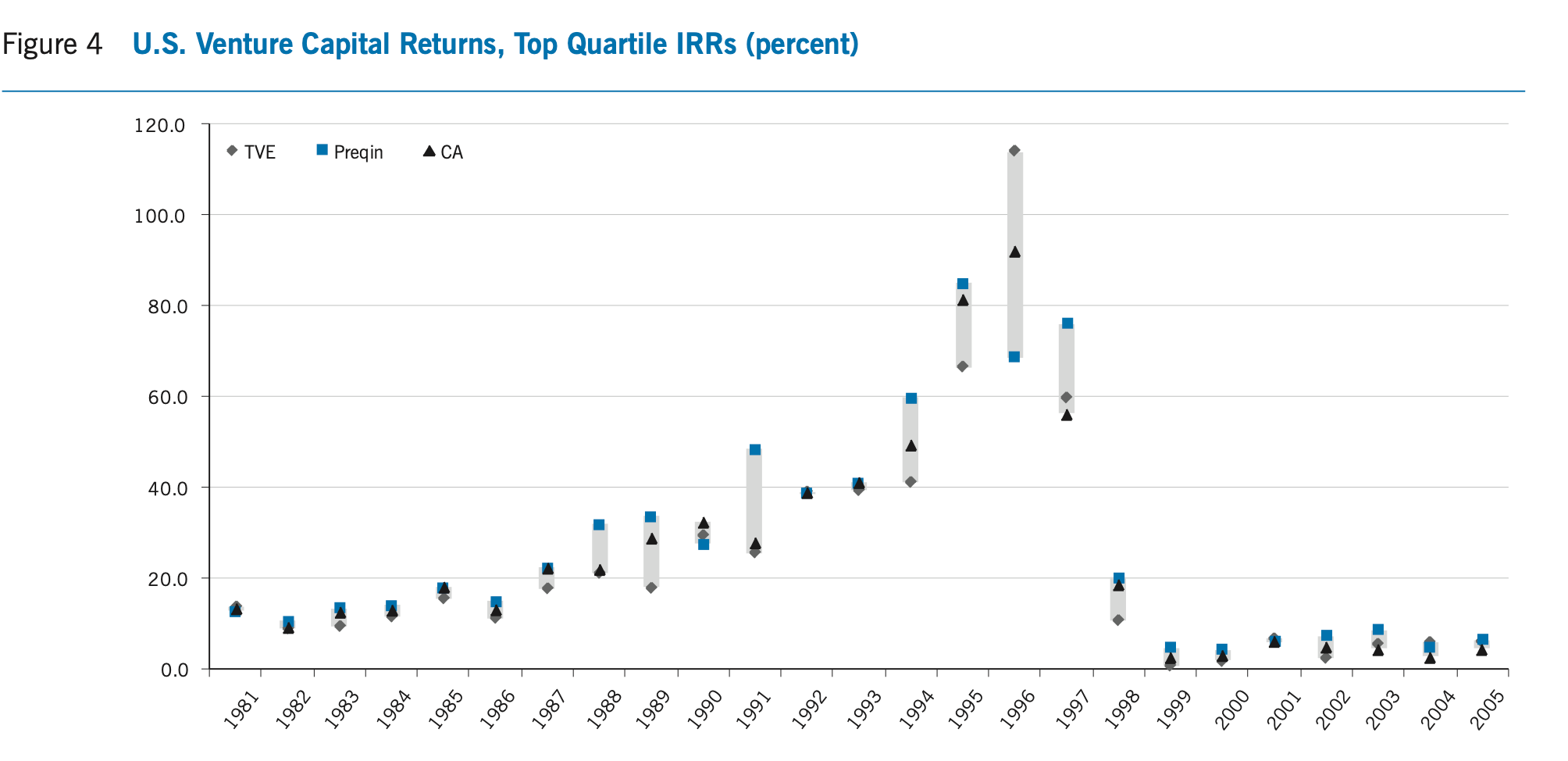

The paper itself is worth is interesting and is well worth a read. That said, from their paper, below are charts that show how IRR differs amongst Cambridge Associates, Prequin, and Thomson-Reuters VentureXpert (TVE).

The dispersion of IRR is pretty massive. In 1995, a median fund according to Cambridge returned above 40%; TVE said that it was 20% or less than half of what Cambridge reported.

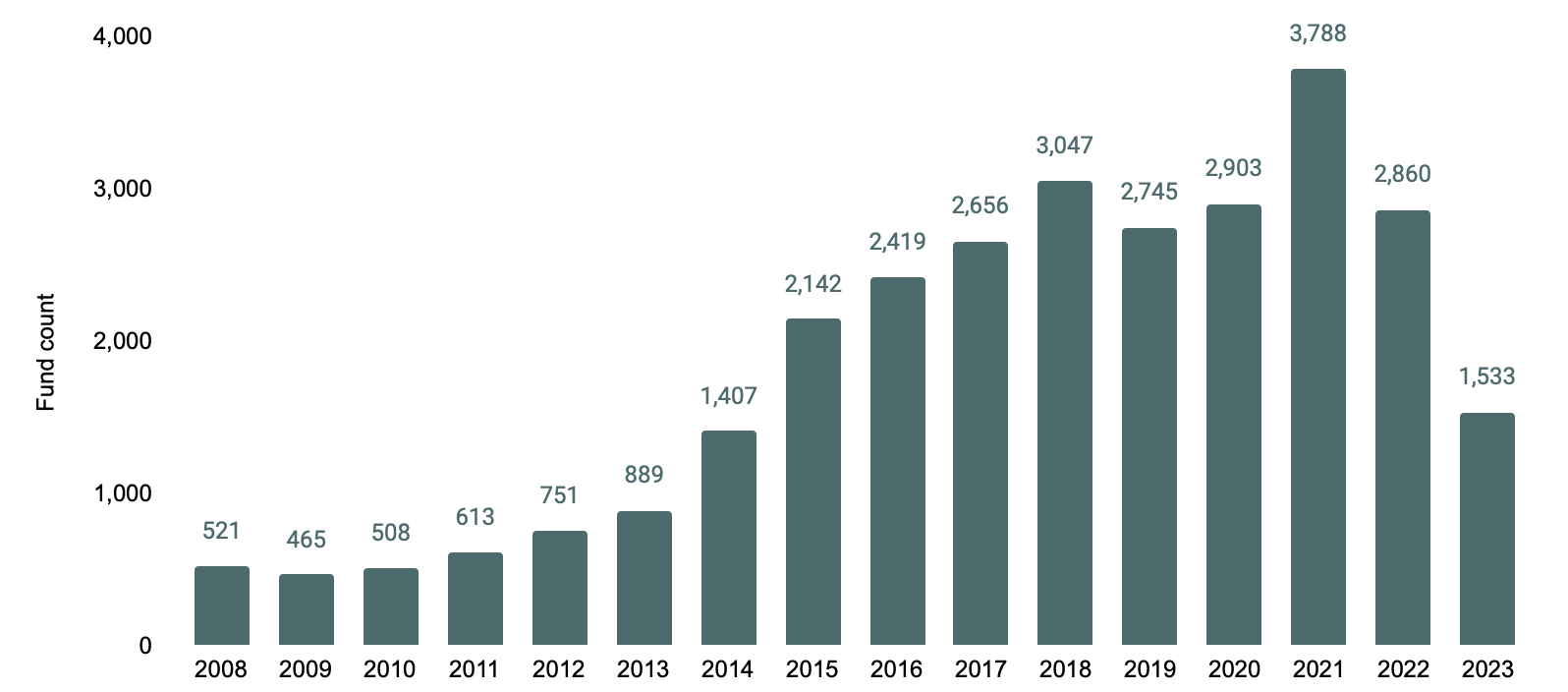

From the same paper, below is the number of funds in a data provider’s benchmark. 2008 has some 55 funds in the Cambridge set. In contrast, I charted Pitchbook data that outlines over 500 funds raised in 2008. In other words, the most comprehensive benchmark dataset has ~10% of the total number of funds raised for its vintage year. Unfortunately, 2008 was the only year in which there was overlap between the two sets of data. But I imagine that it’s not too different for other vintages as well.

Everyone But No One?

Benchmarks are as important as they are not. If everyone is top quartile, then that means that no one is. Raw numbers matter more than the quartile that a fund is in since numbers can jump a lot across vintages. I think the mistake that a lot of (emerging) GPs make is that they are sometimes too focused on their fund’s quartile ranking. A fund’s quartile placement won’t make or break an investment case since they don’t mean anything At best, an actual top quartile track record opens the door to a first meeting-- no more, no less. Plus I rather be an LP in a 2050 vintage with a final 3x DPI in the second quartile than a 2051 fund in the top quartile with a final DPI of 1.2x. Wouldn’t you?

If you have comments, questions, or criticism, message me on Twitter @Lawrence_Ou and I’m happy to chat and discuss! I do put a lot of time into this so if you found this useful, please consider subscribing.

None of the above should be considered fund advice, investment advice, financial advice, or legal advice. It is strictly for informational purposes and is accurate to the extent of the author(s) knowledge. The views and writings above are strictly those of the author(s) and do not in any way represent the views of past or present employers.